Blog

Why Modern Portfolio Theory is useless for wealth planning

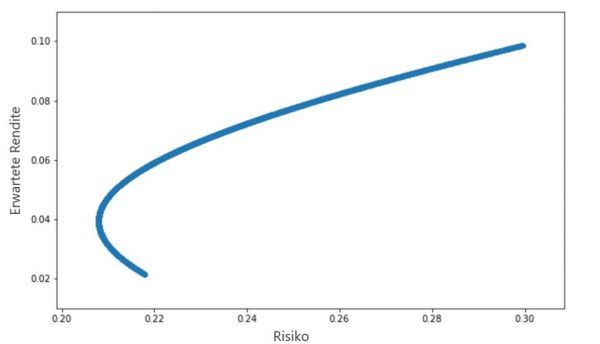

Efficient Frontier according to Modern Portfolio Theory: portfolios with minimal risk at a given expected return.

The result of the MPT optimisation is based on assumptions which are very unstable: Firstly, expected returns are never “spot landings”, but are often far off in practice, as every investor has knows only to well. Secondly, volatility (the standard deviation of returns) is used as a risk measure, which is underestimates drawdowns, especially in crises.

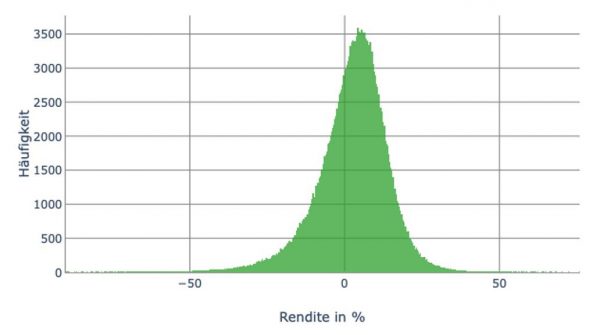

Further, the MPT is based on a normal distribution of capital market returns: Fluctuations are modelled as normally distributed, and the mean corresponds to the expected return. Practical experience shows that a normal distribution simplifies financial markets too much. The reality looks quite different:

Example of non-normally distributed returns: Quarterly return on emerging market equities (1,000 scenarios, 400 quarters)

Furthermore, the MPT Optimisation does not tell Tom if he can actually achieve his financial goals or not: the MPT Optimisation only considers the assets but ignores Tom’s personal balance sheet which includes also liabilities, namely credits and goals. In addition, the optimisation is not robust because small changes in expectations may significantly change the proposed allocation. Finally, the analysis is limited to a single investment period. In financial and wealth planning, however, goals may lie either in the near or distant future and normally have different time horizons. Thus, the consideration of a single investment period is misleading.

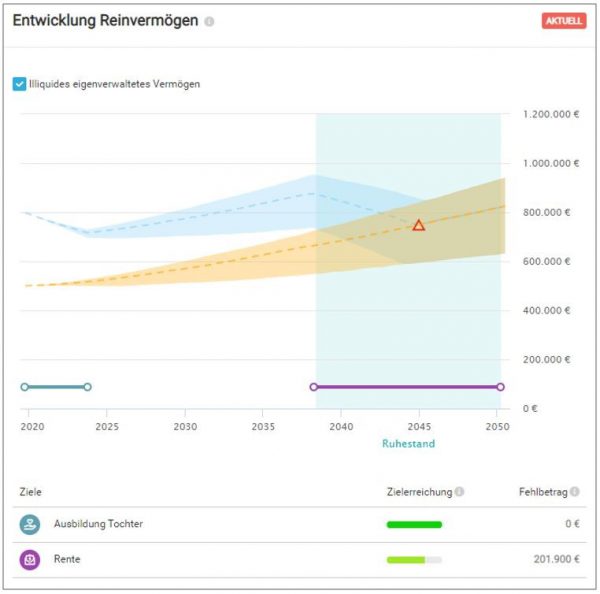

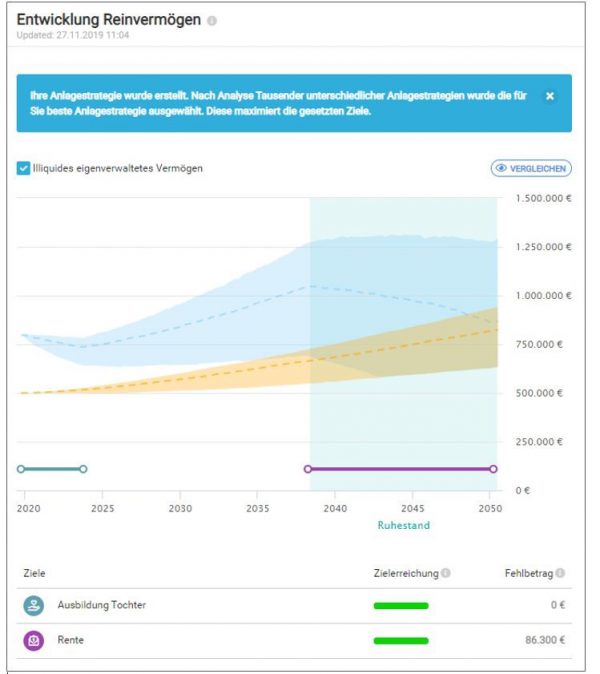

Tom’s optimised goal achievement and wealth development

The likelihood to achieve the second, more demanding goal (to secure the pension of 3,000 euros per month), increases significantly, while the goal achievement of the first goal remains unchanged. Additionally, Tom’s planning becomes more flexible: he can adjust his goals, add new goals and obtain a detailed picture of his financial future. This also includes the simulation of life events such as inheritance, divorce and much more, which can change the financial situation significantly.