Blog

Financial planning as a wealth management service – appreciated by clients, but rarely paid for

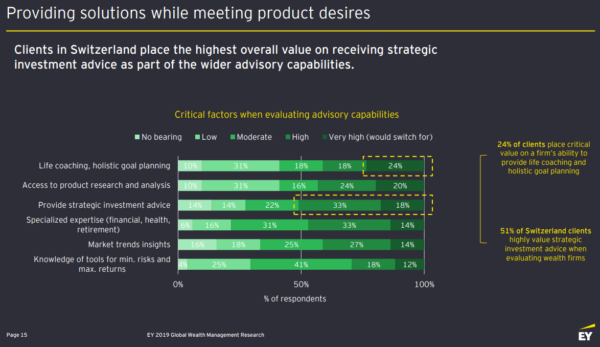

Clients have financial goals, even if they sometimes have difficulty formulating them. This picture changes in most cases once you ask them about their wishes or dreams instead of their financial goals. While our wishes or dreams act as a meaningful inner drive, the financial means for achieving them are – as the name suggests – only a “means to an end”. Negative emotions also play an important role in this respect. For example, the Worry Barometer 2019 of Credit Suisse and gfs.berne puts retirement provision in first place. For this reason, it is not surprising that, according to a study published by EY at the end of 2019, 42% of all clients surveyed in Switzerland are interested (18%) or very interested (24%) in “life coaching & holistic goal planning”, while 51% also want strategic investment advice.

Figure 1: What clients in Switzerland want in terms of advisory skills

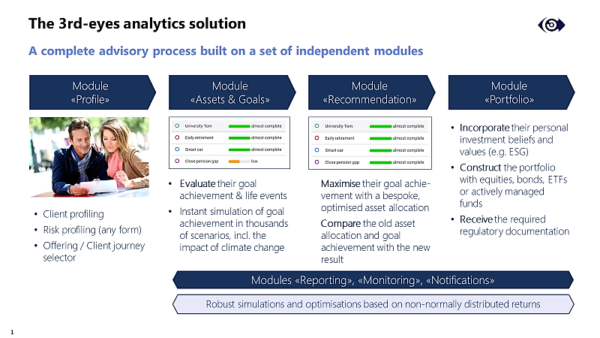

Today, client advisors of banks usually do not have solutions that allow them to easily create forward-looking simulations in the sense of goal-based financial planning. 3rd-eyes analytics offers the adequate solution – either as a supplement to existing advisory solutions or as a full replacement of those.

Figure 2: Entire advisory process of 3rd-eyes analytics

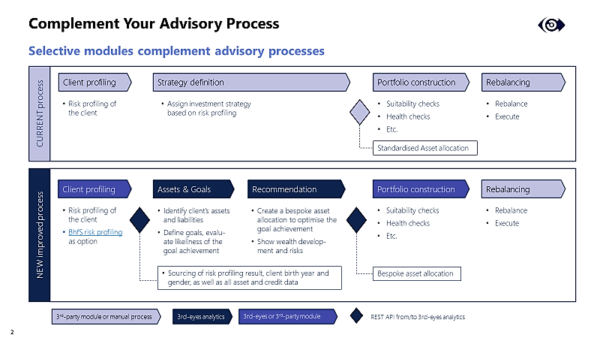

As an alternative to using the entire advisory solution from 3rd-eyes analytics, the existing advisory process is supplemented by the following modules with modern interface architecture (Figure 3).

Figure 3: Extension of the existing advisory process

Module «Assets and Goals»:

First, the overall wealth of the clients, including their goals, is evaluated and the achievement of goals is calculated in thousands of capital market scenarios. All bankable assets, including those with third parties, are considered. This also applies to non-bankable assets as well as inflows, outflows and loans.

Module «Recommendation»

The goal achievement is maximised by seeking the best possible strategic asset allocation (SAA) for each client individually. Unlike the three or five standard SAAs that are normally offered by wealth managers, the basis for this can be either 5, 10, 100 or millions of different SAAs – depending on the bank’s preference. These are each combined with thousands of capital market scenarios. Their goal achievement is then compared to ultimately select the SAA with the highest goal achievement (whereby the optimization function can be parameterized).